Robert Walters Finance Breakfast Speech

New Zealand is not headed in a good direction at the moment.

Our growth rate is too low.

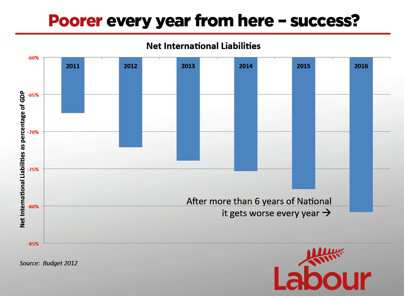

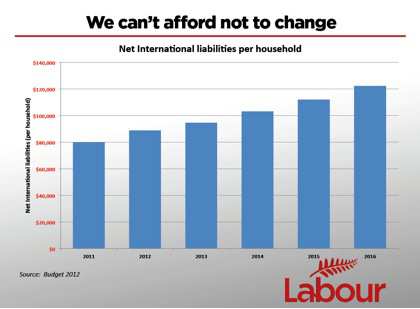

Our overseas liabilities are too high.

We have problems ahead we are not preparing for.

And unless we make some bold changes to modernise our economy, we will continue to drift backwards.

If you scan the headlines of the last couple of weeks you get a picture of an economy that is struggling.

Up to 85 jobs lost at textiles factory Norman Ellison Carpets in Auckland.

Another 70 jobs in Manukau at Flotech, a bio-tech engineering company.

These are good well-paid trades jobs.

Another seventeen workers lost their jobs at a furniture manufacturer in Tauranga.

There are many reasons an individual company might prosper or fail, but we are seeing a pattern here of good jobs being lost in added value export or import substitution businesses.

Growth

Over the past 3 years we have had one of the worst performing economies of any developed country, outside of Europe.

Our major trading partners, Australia and China, haven’t been in recession at all.

It’s not just because of global financial problems and the earthquake that we’ve suffered setbacks.

In fact, we have been slowly drifting behind the rest of the world for decades.

We had a long period of job rich growth in the 2000s, but even that was over-weighted to consumption fuelled by rising international private debt rather than exports.

We have had relatively poor growth for the entire working life of most New Zealanders.

Overseas Liabilities

We have tried to shield ourselves from declining living standards by borrowing and selling assets.

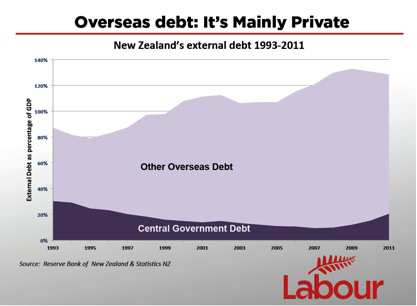

Consequently, our overseas liabilities are among the highest in the world. This is not the government’s borrowing I’m talking about - that’s relatively low, despite the last few years of deficits.

The country as a whole is living beyond our means.

Future pressure

Meanwhile, we are losing 50,000 people a year to Australia. That’s 50,000 fewer people contributing to our economy.

That’s because our wages are too low.

We have a large proportion of the population in low skilled work, or not in work at all.

And ahead of us, the government has fiscal challenges looming, such as the increasing cost of superannuation.

Today there are 5.6 people in the workforce for every retired New Zealander.

In thirty years there will be 2.5.

What this all adds up to is the need to make some changes.

We need to modernise our economy. If we change nothng, nothing will change.

Labour is a party of change

Labour is a progressive party: fundamentally it is the party of change, the party that is willing to make structural changes when necessary.

Our opponents are a conservative party, more or less satisfied with the way things are.

Both have a proud intellectual tradition.

It’s always up to Labour to make the case for why change is needed, and why the status quo isn't working.

So the difference between us is not that the Government is pro-business, and we are anti.

Nor are we talking about ‘tax and spend’, or ‘cutting the pie differently’.

Those are tired cliches.

What we are talking about is the need to modernise because we can’t keep going as we are.

We need to take some hard decisions and shatter some orthodoxies that are past their use-by date.

Our difference with the Government is that they believe they can tweak policy here and there and achieve substantially different outcomes.

Labour’s team

Let me tell you about Labour’s economic team.

I started out in my working life as a lawyer, and I became a litigation and managing partner of Anderson Lloyd, the largest South Island law firm.

I left the law partnership to pursue a range of business interests.

I was manager in the early years of a start up called the A2 Corporation, a high value New Zealand export business that’s based on our competitive strength in agriscience.

I was a co-founder and director of a group of fund management companies. I helped found BotryZen and Pharmazen.

I was GM of BLIS Technologies from start up to the main board of the New Zealand stock exchange, and was involved in a variety of other businesses too.

David Cunliffe, our economic development spokesperson, is a former business consultant from Boston Consulting. They are top shelf.

Shane Jones is a former leader of the NZ fishing industry.

Labour’s leader, David Shearer, has an MBE from the British government for his humanitarian work.

He was the NZ Herald’s New Zealander of the year in 1992 and the UN promoted him to a senior role in Iraq, with a two billion dollar budget rebuilding schools, and hospitals and power stations – testament to his undoubted abilities.

This is a team with senior business experience, as well as ministerial experience of our economy.

It is a team with skills to understand tough problems.

We understand that many of New Zealand’s structural problems are caused or made worse by economic settings that only government can fix.

What we need to modernise

The solutions to chronic debt, low growth and looming fiscal pressures require our economy to be modernised in four basic categories.

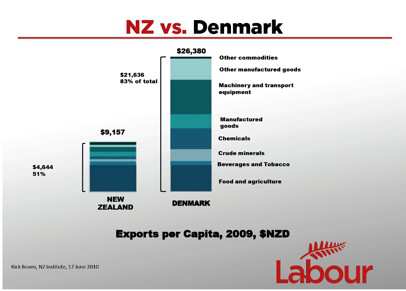

We need to grow our exports, which in turn requires attention to why we are not selling as much overseas as we need to sustain the lifestyle we aspire to.

That means looking at our monetary policy, and looking at the drivers of more high value, high skill innovation.

Second, we need more of our own capital, which requires us to save more and to be prudent about the nature of investment in our economy.

Third, we need to fix the tax system so that we promote growth in exports instead of penalising it.

And fourth, we need to make hard decisions about looming fiscal pressures.

Thriftiness

We have to provide for the future in the interests of all New Zealanders.

Labour is promising to be thrifty. Labour ran budget surpluses for 9 years, leaving the incoming National government with amongst the lowest government debt in the world.

We agree with the Government that getting back into surplus in 2014-15 is a good objective.

One example of being thrifty is superannuation.

In just three years time – super costs more than total government spending on pre-school, primary, secondary and tertiary education combined.

We have to act now to ensure adequate retirement incomes are there for everyone in the future.

By gradually lifting the age over a long-period we can ensure NZ Super is available for everyone and give people time to plan.

So we disagree with the Government that this issue can be avoided.

Passing the buck is reckless and irresponsible. We are more frugal than them, because we are prepared to confront this issue.

We also disagree with the Government that on its own tight economic management is enough to deliver economic success.

The Government cannot claim a successful economy is one that isn’t growing.

We have to focus on growing the economy – especially the productive export economy, and reducing the overseas debt.

Pro-growth tax reform

We’re also being thrifty by being clear about where future revenue is going to come from.

That has to include pro-growth tax reform.

One fundamental lesson I learned in business is that it has long been easier to make money in New Zealand from property, retail or local services than from exporting.

It’s no surprise that’s where so much of the smart money goes - at the expense of our productive export sector.

A capital gains tax would not be a tax grab, but a first step in reconfiguring the tax system to make it more productive.

Investment should go where it is most economically efficient, not where it gets the best tax advantage.

The other limb of pro-growth tax reform is that if our businesses invest in research and development of innovative export products, they get no tax break.

Consequently, our private sector spend on R&D is one third of the OECD average.

Supporting our exporters will keep more profits here and reduce our reliance on foreign borrowing;

Growing our science and innovation investment will result in more new products and ideas to take to the rest of the world.

Then we have to back that up with a new vision for skills, education and training.

Growing a skilled workforce will mean New Zealanders can take advantage of the job opportunities of a 21st century economy.

We cannot push our economy into the global winners’ circle by relying solely on the advantages of a temperate climate.

And there is no future in being merely a destination for low wage investment.

Our future – both for primary industries and beyond – is in our talent, science and innovation.

We must grow the breadth of our exports.

Exports

Innovation is one contributor to increasing our exports.

Another area where we are beginning to hear modernisers question old orthodoxies is in monetary policy.

Our current Reserve Bank Act was passed nearly a quarter of a century ago.

Since then, we have lost control of nearly all our financial institutions.

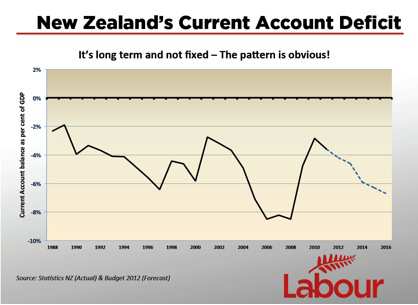

Inflation has been subdued, but our current account deficit is serious and caused mainly by private borrowing, not government deficits.

Our net international liabilities are among the highest in the developed world.

The problem with the current orthodoxy is that no amount of evidence would cause its defenders to say we need to have a new look.

Last month, fifty jobs were lost in Oamaru from Summit Wool Spinners’s textile plant.

This is a plant that adds value to our competitive advantage in agriculture.

In a town of 13,000 people, fifty jobs is going to affect a lot of people.

Those jobs weren’t lost because there is something intrinsically wrong with that business.

It wasn’t in the wrong place or badly run.

They were destroyed by the persistently high New Zealand dollar.

The IMF have looked at our currency, and they say it’s persistently overvalued - currently by about 15 per cent.

Labour is totally committed to Reserve Bank independence, and to a low inflation target.

But if you look at our external debt, New Zealand needs to modernise our economy and orthodoxies need to be re-examined.

Savings and Investment

The fourth area to modernise is savings and investment.

A major part of our current account deficit is already comprised of interest and dividends paid to overseas investors.

Because we don’t save enough we are reliant on imported capital to fund our current account deficit.

Most of this comes via increased lending to home owners.

But our deficit is used by some as a misplaced justification for the sale of all productive assets to overseas buyers.

We need foreign investment, but we cannot lose control of our best income producing assets.

Successful New Zealand companies often rely upon overseas capital to expand.

New capital via foreign owned firms can bring with it new business expertise and higher productivity, access to markets and technology transfers.

What we’ve found is that these benefits of foreign direct investment are strongest when the investment is directed at ‘greenfields’ investment and to the export manufacturing sector.

The merits of FDI in the primary production sector are far less compelling.

Our approach will be to tighten rules around sale of farm land.

Sales will be declined unless there is significant investment in processing and related jobs.

We also think infrastructure assets with monopoly characteristics are especially important to the functioning of the wider economy.

Labour published a closed list of assets that we believe ought to be run in the New Zealand interest because they have monopoly characteristics - assets such as electricity line networks, water and airports.

The list excludes telecommunications and electricity generation

What we need to do instead is save more.

That’s what Australia is doing and one of the reasons they’re racing ahead of us – they already save 9% and are increasing that to 12%.

Last year Labour proposed extending Kiwisaver by enrolling all employees in a universal savings scheme.

We will update the policy but the direction is one we have to move in.

Conclusion

What I’ve laid out for you is a comprehensive sweep of modernising reforms across superannuation, pro-growth tax reform, help for innovation and exporting, and modernising our savings and investment policy.

A modern economy will put more of a priority on innovation and talent.

More investment in science and research, in skills and education all the way through from early childhood to post-doctoral.

A universal savings scheme.

Pro-growth tax reform.

Dealing with the looming fiscal pressures.

Those are the big issues, and if you can tell me one we have let off the list of major changes, I would like to hear it.

The issue we have to face is not wondering what to do; We know we have to change and modernise.

The real issue is whether we are prepared to be bold enough to do it.

Small, incremental and fiddly change won’t be enough

Our economy isn’t a success if it isn’t creating jobs.

It isn’t a success if it isn’t growing more profitable export businesses.

It isn’t a success if means growing overseas debt and wages falling further behind Australia’s.

The economy has to grow for everyone.

It has to grow for businesses waiting for the upturn.

It has to work for the men and women who go to work each day, do their bit, and miss out on the gains.

It has to work for our children coming through.

That’s what Labour will be working for.